Monsoon Risk Intelligence Platform

Predict textile stock

volatility from rainfall

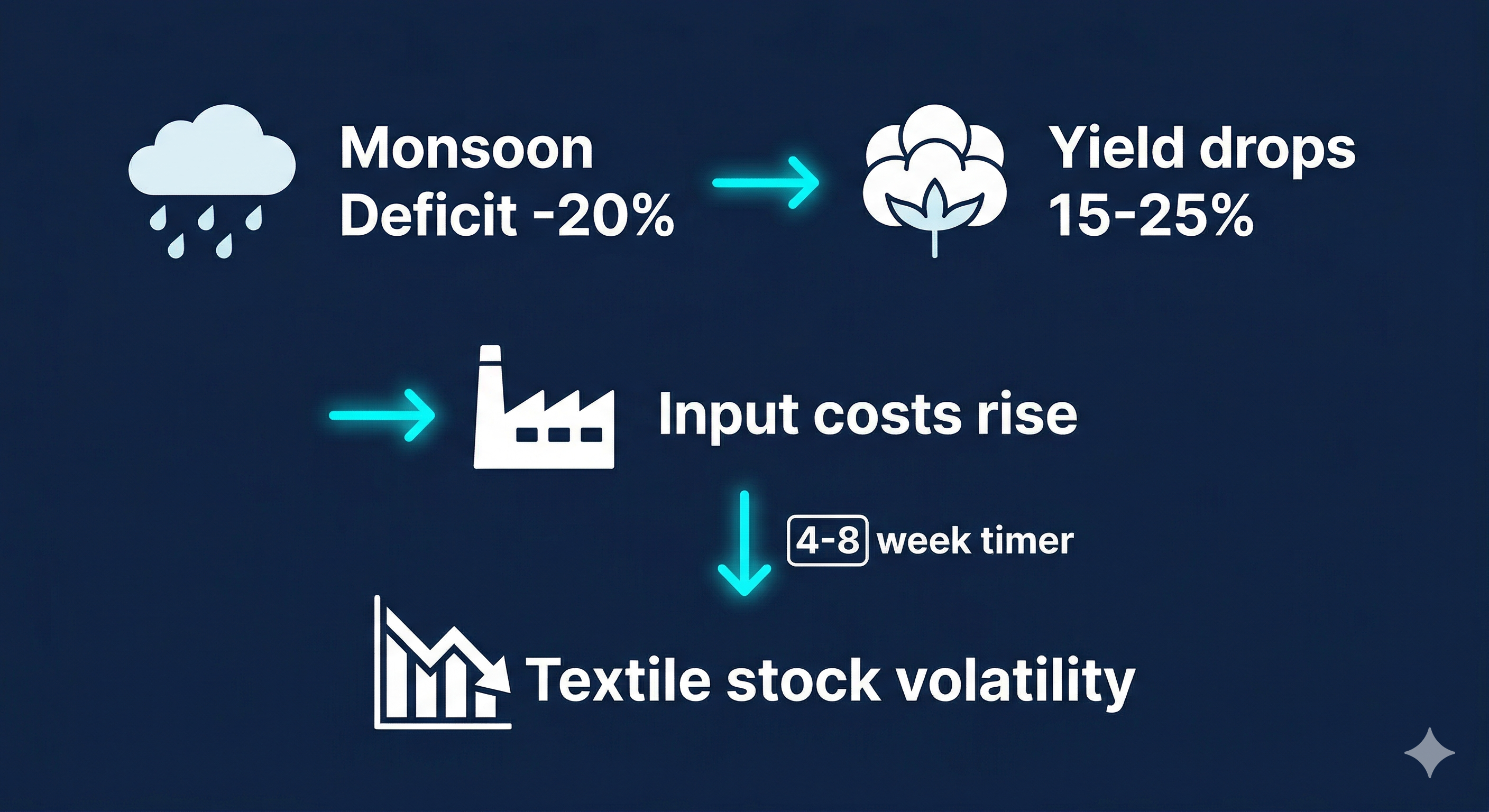

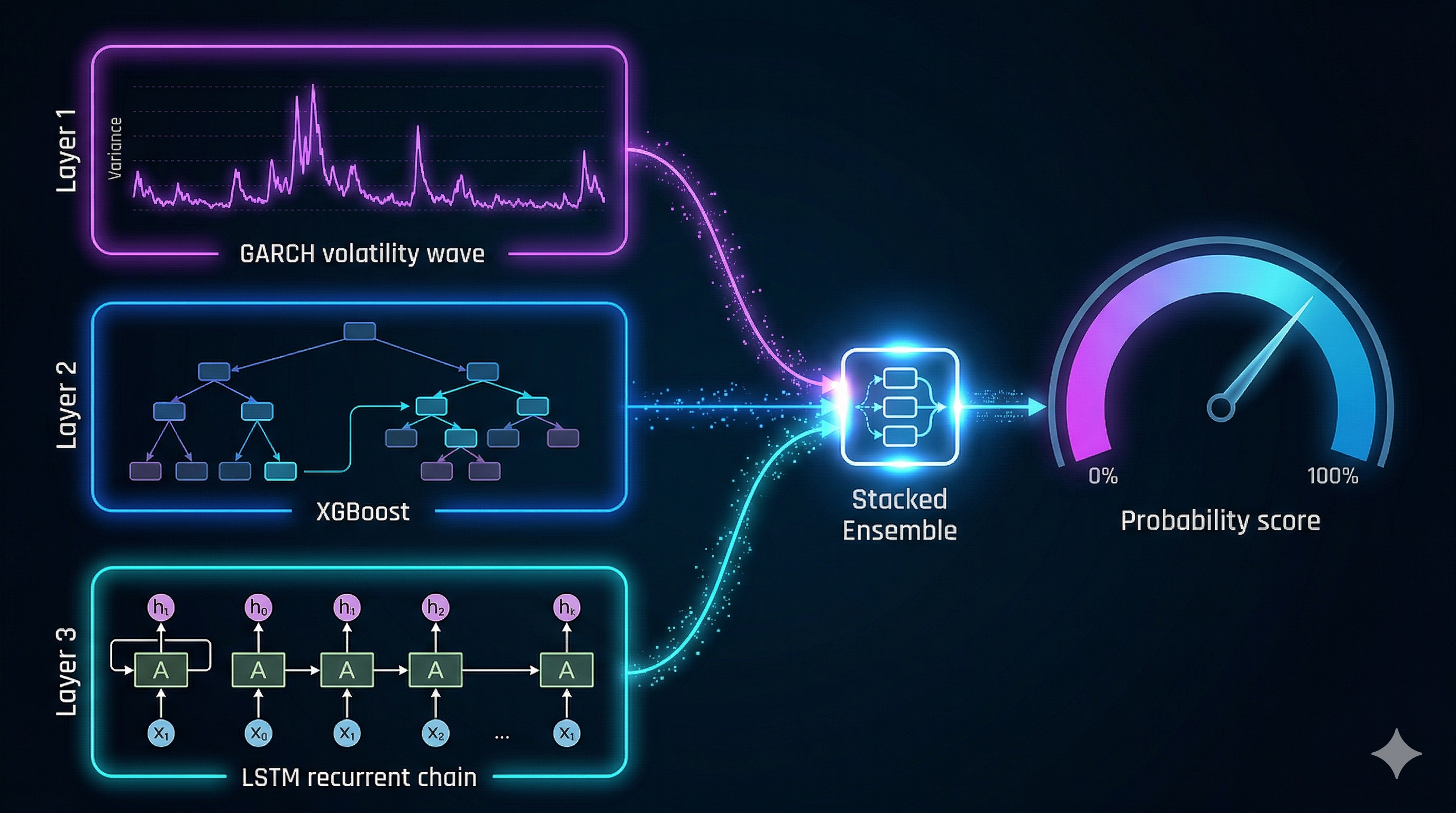

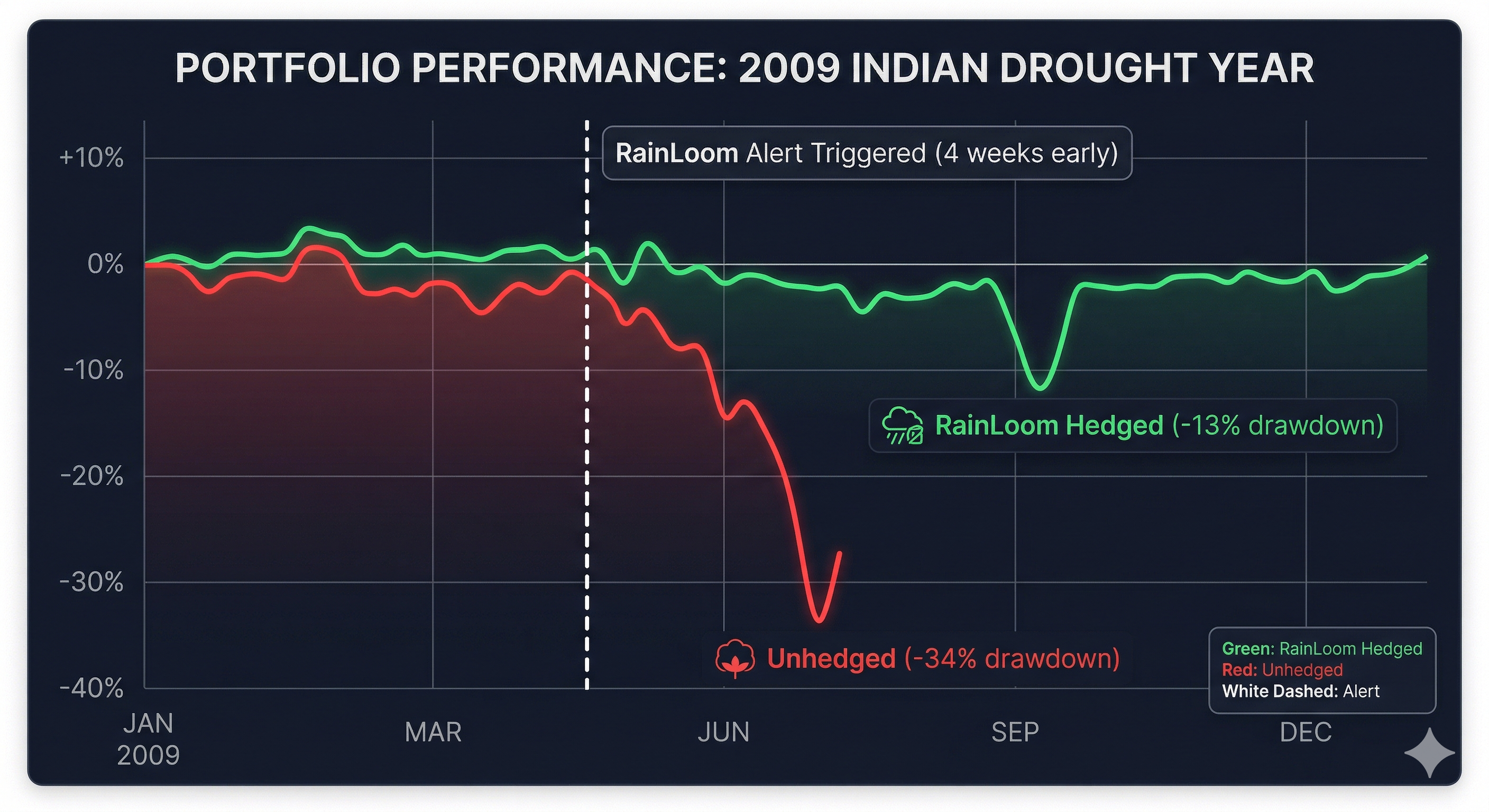

RainLoom connects monsoon failures to cotton prices to textile margin squeezes — giving portfolio managers a 4-week lead time on volatility spikes with AUC 0.81 accuracy, plus live alerts, geospatial nowcasts, and an institutional API layer.

0.81

AUC-ROC

8

NSE Stocks

83

Districts

4 wk

Lead Time

5.8

F-Stat (IV)

18-24%

Hedging Alpha